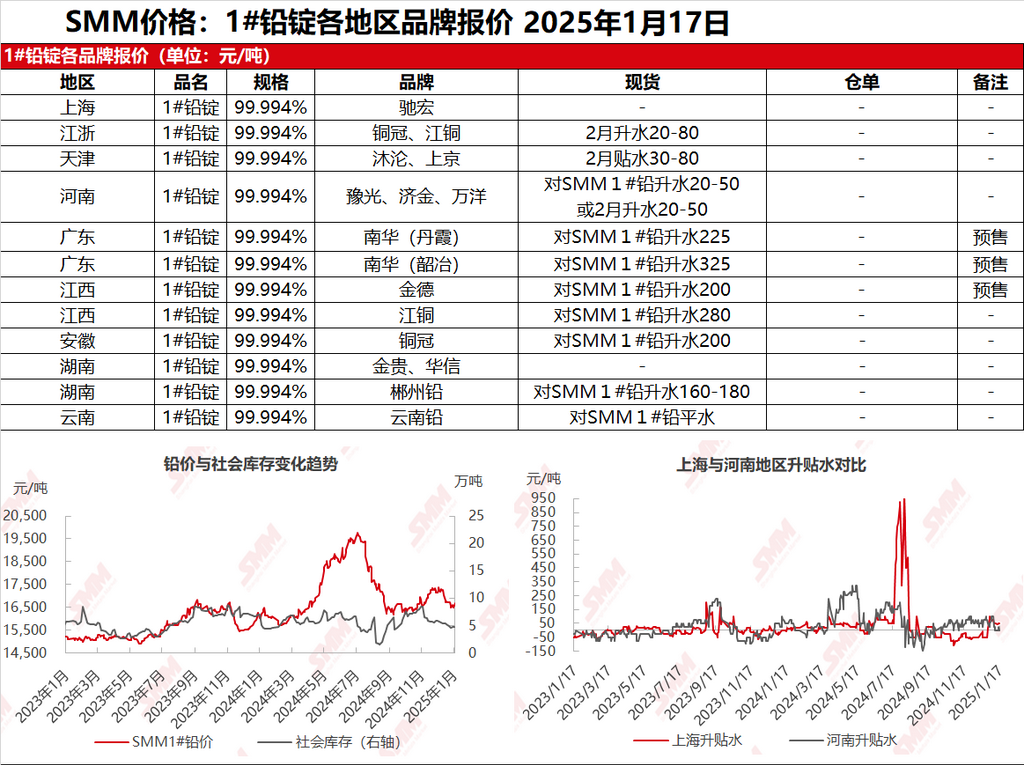

SMM, January 17: Quotations in the Shanghai market were scarce; in Jiangsu and Zhejiang regions, Tongguan and JCC lead were quoted at 16,730-16,830 yuan/mt, with a premium of 20-80 yuan/mt against the SHFE lead 2502 contract. Driven by favourable macro news, non-ferrous metals generally rose, and SHFE lead fluctuated upward. Suppliers followed the market trend in selling, but as the Chinese New Year holiday approached, the spot market showed a stronger festive atmosphere, with reduced transportation vehicles and rising freight costs restricting spot transactions. Additionally, as downstream enterprises were about to go on holiday and lead prices increased, some enterprises abandoned their pre-holiday low-price restocking plans, turning to a wait-and-see approach or directly canceling their restocking plans.

Other markets: Today, SMM #1 lead price rose by 100 yuan/mt compared to the previous trading day. In Henan, long-term contract cargo pick-up remained dominant, and suppliers stood firm on quotes with a slight premium over SMM #1 lead, while downstream transactions weakened. In Hunan, premiums remained at 150-200 yuan/mt, with downstream maintaining just-in-time procurement. Meanwhile, in Jiangxi, Yunnan, and Guangdong, primary lead supply had not yet recovered, and smelters mainly offered pre-sale quotations. Downstream pre-holiday just-in-time restocking was nearing completion, and transactions gradually weakened.

![Imported Refined Lead Arrivals Increase, Smelters Add New Maintenance Plans in April, Lead Prices Are Expected to Maintain a Fluctuating Trend in the Short Term [Brief Commentary on Lead Futures]](https://imgqn.smm.cn/usercenter/LCtEk20251217171721.jpeg)